Late payments are not just an inconvenience for small and medium enterprises across Africa. They are a survival threat. When customers delay payment by 30, 60, or 90 days beyond agreed terms, the ripple effect touches every part of the business — from the owner’s ability to pay suppliers and staff, to the capacity to take on new orders and grow.

The frustrating part is that many of these late payments are not caused by customers who cannot pay. They are caused by operational gaps on the seller’s side: invoices sent late, invoices sent with errors that trigger disputes, and a lack of systematic follow-up that allows overdue accounts to drift.

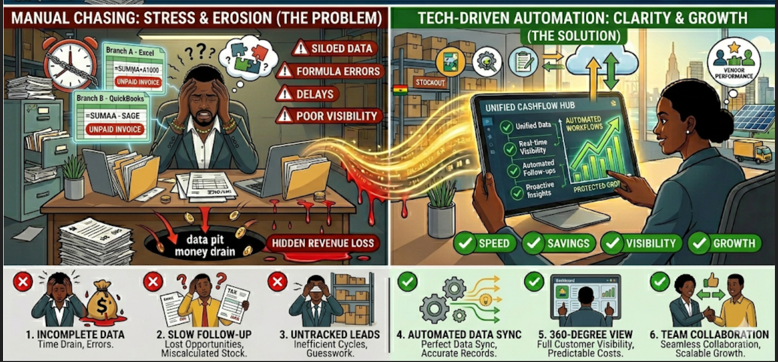

For most African SMEs, the late payment problem is not a credit risk problem. It is a workflow problem. And workflow problems have workflow solutions.

Where Businesses Go Wrong: The Receivables Blind Spot

In most SMEs, the invoicing and collections process works roughly like this: finance generates an invoice after a sale is completed. The invoice is emailed or delivered. Then the business waits. If the customer does not pay on time, someone — usually the owner or a finance manager — sends a reminder. Maybe a phone call. Maybe a WhatsApp message. The follow-up is ad hoc, based on memory and urgency rather than a systematic process.

Meanwhile, there is limited visibility into the overall receivables picture. The aging report — if one exists — lives in a spreadsheet that is only as accurate as the last time someone manually updated it. Partial payments are hard to track. Payments received at one branch are not immediately visible to head office. And the true cash position of the business is a moving target.

A Scenario You Might Recognise

Mensah runs a food distribution company in Tema, supplying restaurants and hotels across Greater Accra. His terms are 14 days net, but his actual average collection time is closer to 35 days. He knows this because he calculated it once, six months ago. He suspects it has gotten worse.

Mensah’s bookkeeper maintains an aging spreadsheet that gets updated every two weeks. In between, payments arrive to the company’s mobile money account, the bank account, and sometimes in cash at the warehouse. Reconciling who has paid and who has not requires cross-referencing bank statements, mobile money records, and the bookkeeper’s spreadsheet. By the time Mensah has a clear picture, some invoices are already 45 days overdue.

Last quarter, Mensah discovered that one of his largest customers had an outstanding balance of GHS 28,000 — spread across seven invoices over three months. Nobody had followed up systematically because each individual invoice seemed manageable. The aggregate exposure only became visible when Mensah manually compiled the data.

What This Is Costing You

Cash You Cannot Use

Every day a receivable sits unpaid is a day your cash is trapped. For SMEs without large cash reserves, this creates a dangerous dependence on supplier credit or short-term borrowing. Businesses that improve their days-sales-outstanding by even 5 to 15 days unlock working capital that can fund operations, inventory, and growth without additional borrowing.

Time Spent Chasing Instead of Growing

Finance teams in SMEs often spend 30 to 60 percent of their time on manual payment follow-ups — sending reminders, making calls, reconciling payments, and resolving disputes. This is time that should be spent on forecasting, analysis, and strategic financial planning.

Supplier Relationships Under Pressure

When your customers pay you late, you pay your suppliers late. This strains supplier relationships, costs you early-payment discounts, and in extreme cases can lead to supply disruptions. The late payment chain is circular, and SMEs often find themselves at the most vulnerable link.

Business Failure Risk

Cashflow problems are the leading cause of small business failure. Not lack of demand. Not poor products. Simply running out of cash because receivables are not collected efficiently. Industry surveys across Africa and globally consistently show that a large majority of SMEs struggle with overdue invoices, and for some, the impact is existential.

A Better Way to Operate: Receivables as a Workflow, Not an Afterthought

The fix is not chasing harder. It is building payment collection into your operational workflow so that it happens automatically, consistently, and with full visibility.

This means invoices that are generated and delivered instantly when a sale is completed — not days or weeks later. It means automated reminder sequences that follow up at defined intervals without anyone needing to remember. It means a receivables dashboard that shows every outstanding invoice, every partial payment, every overdue account, in real time, across all branches.

When receivables management is embedded in the workflow rather than handled reactively, businesses typically see overdue invoices drop by 20 to 50 percent and collection cycles shorten materially.

How Webhuk Turns Receivables Into a Controlled Process

Webhuk integrates invoicing, payment tracking, and receivables management into its core operational workflow. When an invoice is generated — from a sales order that traces back to an original quotation — it enters the receivables pipeline automatically. Payment status updates in real time as receipts are recorded, whether received by bank transfer, mobile money, or cash.

The receivables dashboard gives finance a live view of all outstanding amounts, broken down by customer, by age, and by branch. Configurable reminder workflows can be set to automatically follow up at defined intervals, removing the reliance on manual tracking and memory.

For businesses with multiple branches, all payment data consolidates into a single view. A payment received at one branch is immediately reflected in the central receivables record, eliminating the reconciliation gap that causes many SMEs to lose track of overdue amounts.

The result is faster collection, fewer bad debts, and finance teams that spend their time on analysis rather than detective work.

Ready to stop chasing payments? Try Webhuk free for 7 days and take control of your receivables.

Learn more: How the Full Invoice-to-Payment Workflow Works in Webhuk

Frequently Asked Questions

What is days-sales-outstanding (DSO) and why does it matter?

DSO measures the average number of days it takes to collect payment after a sale. A lower DSO means faster cash collection and healthier working capital. Even a modest improvement of 5 to 15 days can free up significant cash for an SME.

How do late payments affect small businesses in Africa specifically?

African SMEs often operate with thin cash reserves and limited access to credit. Late payments create a chain reaction: inability to pay suppliers on time, missed growth opportunities, and in severe cases, business closure due to cashflow collapse.

Can Webhuk send automatic payment reminders?

Yes. Webhuk supports configurable reminder workflows that automatically follow up on outstanding invoices at intervals you define. This removes the dependency on manual tracking and ensures consistent follow-up.

Does Webhuk track partial payments?

Yes. Partial payments are recorded against specific invoices, and the remaining balance is updated in real time on the receivables dashboard. This gives finance complete visibility into payment status at all times.

Can I see receivables across all branches in one place?

Yes. Webhuk consolidates receivables data across all locations into a single dashboard, so head office can see the full picture without waiting for branch-level reports.